My latest article for Worthwhile Magazine™ is a series of questions to consider asking yourself while contemplating a new addition to your art collection. Often I’m on the scene as an appraiser only after a purchase has been made, so the following group of prompts is based on lessons clients have shared with me about what informs their buying process, or what they wish had! My article is below or you can also read it online at Worthwhile Magazine™:

“It’s no secret I am passionate about the topic of helping people build a cherished collection of items they love living with—their right stuff. It can be quite difficult to evaluate a new potential purchase clearly to discern what course of action would truly reflect your deepest wishes when confronted with the physical experience of a beautiful artwork and a very agreeable gallery representative eager to work with you. Below I’ve compiled some questions based on my years of observation and experience in the field that may be helpful to consider asking yourself as you work to sort out your thoughts and feelings regarding a new potential future purchase. Some questions may resonate more than others, and that’s perfectly fine. My hope is the structure of inquiry and analysis will help you move forward feeling confident about your decision, whether it is to go ahead with a purchase or hold off.

QUESTIONS TO CONSIDER:

-Do I love this piece?

-Why am I drawn to purchase this piece?

-Did a gallery or art dealer or consultant tell me I should purchase this piece?

-Do I feel like I’ll be perceived as more sophisticated and worldly by having this piece displayed in my home?

-Have I checked out the reputation of the venue I’m working with? Do they have any legal cases against them or any controversies in their history?

-Does the venue have any independent consumer ratings available to review?

-What is the return policy at the venue I’m working with? Do they have an option to test out the work in my home before committing to purchasing it?

-Where does the venue source the work I am considering? Is it directly from the represented artist or the artist’s estate or is the sourcing not disclosed?

-Is the venue’s pricing reflective of its level of the market, or is it significantly out of range in either direction?

-What sort of provenance paperwork will the venue provide?

-Am I concerned about potential future monetary appreciation of the work, or will I simply enjoy looking at it?

My latest article for Worthwhile Magazine™ tackles a tricky area of appraising: understanding the different levels of value. This is one of the most confusing elements of appraising that I spend a lot of time discussing with clients, so I wanted to cover the subject in an article that could reach and help a much broader audience. The following is my article or you can also read it online at Worthwhile Magazine™:

“One of the most challenging things to wrap my head around during my formal training to be an appraiser was that value and worth as we popularly understand it in our culture are completely relative. There is immense curiosity regarding the question “what’s this worth?” but an appraiser’s answer is usually some form of “it depends.”

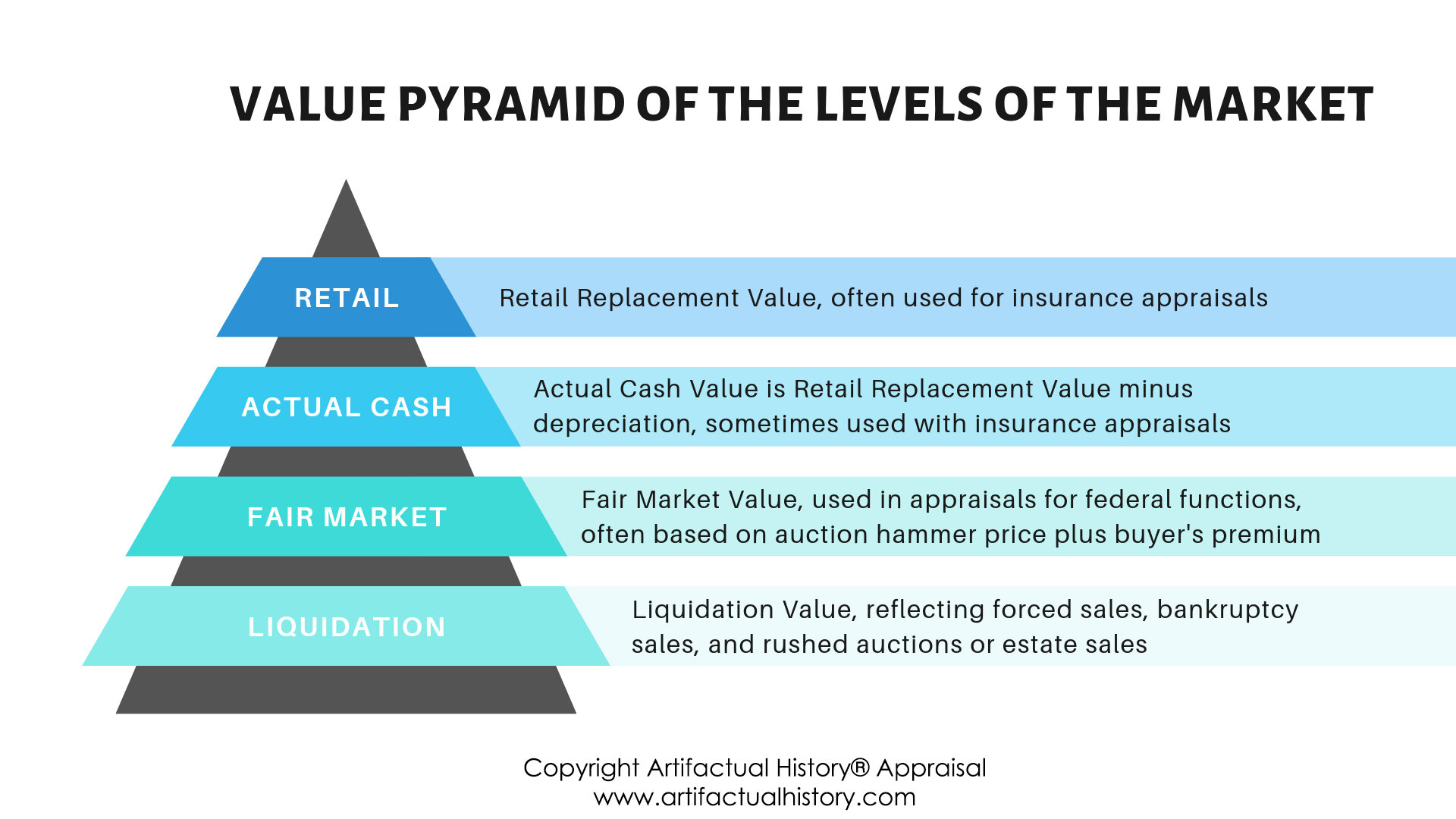

Value exists in the presence of its context in a specific level of the market at a specific point in time.

Without those other two data points of 1) market level and 2) point in time (which is commonly referred to as the “effective date,” meaning the date the appraised value is effective for), any number that is thrown around as a value is essentially meaningless.

Based on this, the same exact object can have multiple values on the same day, depending on what level of the market one is evaluating. An appraised value for insurance may be significantly higher than an appraised value for planned future sale, which can be baffling and difficult to comprehend without a familiarity with the different levels of the market.

For those without dedicated appraisal training, and especially for those in the general public who may be thinking of having items appraised, these concepts are often unknown and frequently very confusing. I’ve written this basic guide as an introduction to the different levels of value so that users of appraisal services will be able to better determine what sort of appraisal reports would best suit their needs. To be clear, the levels I am describing are those typically used in the United States, where I am based, but I recognize that among our international readership there may be other levels of value specific to different countries.

All appraisal reports written in compliance with the Uniform Standards of Professional Appraisal Practice (USPAP) have to include identification of the level of the market the appraised values are set in and the effective date of the valuation. There are a number of professional organizations for appraisers, and regrettably, they don’t all use the same terminology to describe the different levels of the market. For the purposes of this guide and to improve clarity for a general audience, I have streamlined and simplified some of the names of the market, particularly for the retail market, but readers should be aware that their appraiser may use slightly different terms depending on that appraiser’s professional memberships.

Below I will introduce the different major levels of the market working from highest to lowest, and discuss the appraisal purposes, or intended uses, that are frequently associated with certain market levels. While there are a number of other rarely used levels, in this guide I’ve focused on the main, most commonly used levels.

As defined by the Appraisers Association of America, appraised "retail replacement value" is defined as the highest amount in terms of US dollars that would be required to replace a property with another of similar age, quality, origin, appearance, provenance, and condition within a reasonable length of time in an appropriate and relevant market. When applicable, sales and/or import tax, commissions and/or premiums are included in this amount.” (Appraising Art: The Definitive Guide to Appraising the Fine and Decorative Arts, 2013, Appraisers Association of America, page 438.) You may also see this level of the market described as “replacement cost,” which is a term used by the International Society of Appraisers.

Examples of retail replacement value are the price an art gallery asks for a painting in their inventory, the asking price of a table by a furniture designer, or the manufacturer listed price of a sterling silver serving item. The key elements of the definition of retail replacement value are “the highest amount… that would be required to replace a property with another of similar [characteristics] within a reasonable length of time.” This is because retail replacement value is typically used in insurance appraisal reports, and in the event of loss, the client needs to receive a settlement from the insurance company that is sufficiently high to replace the lost items with similar replacements in a relatively short time frame. The best availability of inventory to accomplish this is within the retail market. While it might be possible to scour the auction market for years searching for an offering similar to the lost item and then obtain that item at a much lower price, this is not the function of insurance coverage. Clients pay the insurance premium precisely to preserve the option of receiving a settlement sufficient to replace items within a practical time frame sourcing from the retail level of the market.

Due to these factors, retail pricing tends to be much higher than the other levels of the market, and it can contribute to misleading expectations of the profit in a planned future sale if retail replacement values are the assumed future sale price. Most people selling items on the secondary market who aren’t professional dealers or without access to the assistance of professional dealers will find it difficult to obtain retail prices in a sale, and can more realistically expect future sale prices to be closer to the Fair Market Value and Liquidation Value levels of the market. Part of the reason retail prices are so much higher than the other levels of the market is that they reflect the overhead and carrying costs of the gallery or dealer maintaining the instant availability of the item. A gallery may have to wait years before selling a painting in its inventory, and in that intervening time the gallery would be paying rent or a mortgage for the gallery space, utilities, taxes, advertising, employee payroll, and insurance for the works in the gallery’s inventory. All of those costs are factored into retail prices and contribute to their position at the top of the levels of the market.

The next level down of value is Actual Cash Value. Actual Cash Value is Retail Replacement Value minus depreciation, which can be a deduction made for age, damage, or another factor. It can sometimes be present in insurance policies, although in my experience it is much less frequently encountered. The best way to determine what level of value you have in your own insurance policy is to pull out and read your policy documents or call up your insurance agent to confirm. In my firm’s appraisal assignments, I’ve found that Retail Replacement Value is the main level of value used in fine art and antique insurance coverage.

The next level is Fair Market Value. Fair Market Value is used in all appraisal reports for United States government federal functions such as non-cash charitable contributions for income tax deductions and estate tax. Fair Market Value is also frequently encountered in equitable distribution and family distribution appraisal reports. The formal definition for Fair Market Value is defined by the United States government as “Appraised "Fair Market Value" is the IRS definition as stated in the Treasury Regulation Sections 1.170A-1 (c) (2) is "the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts." [Source: Treasury Regulations Sections 1.170A-1 (c) (2)]. Fair Market Values are most commonly interpreted as being sourced from auction sold prices, and based on the Technical Advisory Memorandum 9235005 [May 27, 1992], fair market value should include both auction hammer price and buyer's premium.

So what does this mean in plain language if you aren’t familiar with the auction world? The following is the example I use with clients:

Imagine you are watching an auction, and the auctioneer is up at the podium holding a wooden gavel selling a particular item. The auctioneer takes bids from all the bidders interested in the item, and the numbers of the bids continue to climb until there is a single final winning bidder. The auctioneer hammers down the wooden gavel and shouts, “Sold! $400 to Bidder A.” That $400 is called the hammer price, referencing the tradition of the wooden gavel. If Bidder A wants to remove the item from the auction house, in most circumstances it is going to cost more than $400 to be able to do so. Most auction houses also charge what is called buyer’s premium, which is a surcharge on top of the hammer price paid by the winning bidder. 25% is a common buyer’s premium across the industry. In this imagined scenario, Bidder A pays $400 plus a buyer’s premium of 25% of $400, which is an extra $100. When Bidder A pays, the total hammer price plus buyer’s premium will be $400 + $100 = $500. Sales tax is not included in the calculation of fair market value, although Bidder A may have had to pay it!

If you believe you need an appraisal written at fair market value for a legal use such as equitable distribution or family distribution, I recommend confirming this with the lawyer representing you before engaging an appraiser, as well as establishing the effective date the appraiser must write the report to. The website of the Internal Revenue Service also contains a wide range of publications providing detailed guidance about their requirements for different situations.

The final level of value to be discussed is Liquidation Value. This is the lowest level of the market discussed here and represents the price realized in a forced sale within a short time that is lacking adequate advance marketing. Due to the rushed timeline and the limited buyers who would be informed of the sale at short notice, prices are very low. A critical difference between a sale at liquidation value and a sale at fair market value is that the liquidation value sale does not have a willing seller, but rather one who is forced to sell by extenuating circumstances. Liquidation Value is often used in bankruptcy contexts.

If you aren’t sure which level of value you need an appraisal report written at, I recommend discussing your needs with the appraiser you are engaging for guidance. Many of my clients reach out to me not quite sure what they need and our subsequent discussion of the appraisal scope of work clarifies what type of report will be best suited for their situation. Users of appraisal services should feel empowered to actively ask questions about how their needs can best be met.

“Many people are familiar with the concept of insurance coverage in the context of car insurance or travel insurance, but knowledge about insurance coverage of personal property such as fine art or antiques is much less widespread. In my own appraisal firm, I answer many questions from potential clients who are unsure if they need an insurance appraisal report or what the process is to get one. I’ve written this article as a general guide to help empower consumers with knowledge about insurance appraisal reports. It incorporates many of my most frequently asked questions and answers. This guide is designed to help readers determine whether they really need an insurance appraisal report, and if they do, what the typical process is for working with an appraiser to have one prepared.

The world of personal property insurance is filled with all sorts of fun vocabulary like ‘inland marine policy,’ ‘blanketed,’ and ‘rider,’ none of which really make any sense unless you work in the field and are familiar with their specific meanings. I’m going to get to all these terms and define them later, but the very first thing I always recommend in my conversations with potential clients is for them to pull out their current insurance policy and check the coverage. Some homeowners policies can already be sufficient for strong coverage of all items in the house, and a written appraisal report for itemized coverage may not be necessary. The best first step is to confirm what coverage you already have.

Sometimes clients can’t find their policy documents or may not have ever received the full paperwork describing their specific coverage details. In those instances, I recommend they call their agent or local insurance office to ask what their policy covers and confirm their current level of coverage. In my experience, the insurance agents are very pleased to hear from the clients and will take time to explain what their current policy covers and what options they have for adding to it. Even if the potential client finds out an appraisal is not needed, it makes me happy as an appraiser to be able to help. The client now has peace of mind of knowing they are already well-protected and don’t need to move forward with engaging me to prepare an appraisal report.

If you find you do need an appraisal report, how to get one? I recommend searching for an appraiser who is USPAP-compliant and who has a strong connoisseurship background in the types of items you need to have appraised. The “Find a Member” search tool on the websites of the major professional organizations for appraisers (International Society of Appraisers, Appraisers Association of America, and American Society of Appraisers) can help you locate an appraiser whose service area is close to you.

Insurance agent Andrew Elliott, CLU states, ‘In our office, we highly encourage our clients to obtain appraisals for high-valued items or even sentimental pieces passed down through family generations. Whether the item be jewelry, fine art, or antique furniture having a detailed appraisal report allows our clients to feel comfortable with their insurance policy coverage and provides guidance when there is a claim. If no recent appraisal exists after there is a loss such as a fire, then it is very challenging for the property owner to replace or restore the item(s) and the insurance company to settle their claim. If you have questions or would like us to review your options for coverage with our office then please feel free to reach out by email to andrew@myfairfaxinsurance.com.’

After checking their policy documents or talking with their insurance agent, if clients do need a written appraisal report to obtain an appropriate level of insurance coverage for the art, antiques, and other personal property in their collection, when they call me the next step I recommend is to find out what their scheduling threshold is. A ‘scheduling threshold’ is another insurance world phrase that can be confusing, but what it basically means is the amount of money an item must be worth to require that an insurance appraisal report is needed to protect it with insurance coverage. Any item that falls under a scheduling threshold could be protected with blanketed coverage based on the property class or scheduled individually at its value without an appraisal requirement. Sometimes, the insurance company could use a detailed receipt or invoice for an item to schedule it at its valued amount.”

“Worthwhile Magazine™ is an online repository of personal property appraisal knowledge accessible to the general public and professionals alike. Discussions include evolving practices and current scholarship used when valuing the various fields of collecting. Since knowledge is power, we believe an open dialogue about connoisseurship is worthwhile.”

As part of our goal of increasing empowerment, access to the magazine’s content is free and open to both industry professionals and the general public.

We have an exciting group of content planned for the coming year to expand on the articles already published in 2018. Our existing content includes:

You can check out all of our articles and read them in full online at https://www.worthwhile-magazine.com/articles-page/ and if you are interested in submitting a contribution or know someone to recommend, our Submissions process and Content Style Guide can be reviewed online herehttps://www.worthwhile-magazine.com/submissions/ You can also subscribe to receive notifications of newly published articles.

It has been a deeply rewarding and fun experience to create the magazine with Courtney, and we look forward to expanding our “open dialogue about connoisseurship” in the coming year.

In addition to co-founding the magazine, it was quite an eventful year here at the appraisal firm, with a number of professional milestones achieved. Among other accomplishments, this year I successfully completed the requirements to reach the “Certified” level of membership in the International Society of Appraisers, which is their highest and most prestigious level of membership. I can now add “ISA CAPP” following my name in recognition of that membership level, and I am among roughly 20% of all ISA members who have met these requirements and completed the process.

This summer I also had the opportunity to apply and gain acceptance in a new professional designation offered by the International Society of Appraisers, the “Private Client Services” designation for working with high-net-worth individuals. Obtaining this designation involved taking a two-day workshop called “Appraising in the World of High-Net-Worth Individuals “ which featured talks by experts specializing in the administration of the complex legal and accounting infrastructure of high-net-worth individuals. The workshop included presentations by trust attorneys, insurance agents, curators of private collections, and family office managers. I found it very informative and particularly appreciated the discussion of new tax changes and their implications for users of appraisal services. In addition to participating in this workshop, appraisers had to meet a number of extra requirements from a list of criteria to obtain the “Private Client Services” designation, such as having a master’s degree, regularly working with high-net-work commercial clients such as financial planners, estate attorneys, and museums, publishing professional articles, and appraising over $1,000,000 in fine art or $500,000 in decorative arts per year over the past three years.

My continuing education also included attendance at the Foundation for Appraisal Education’s annual seminar and my 7-Hour Update course for the Uniform Standards of Professional Appraisal Practice (USPAP) that I must take every two years to remain a USPAP-compliant appraiser. I gave several presentations about appraising and had a very interesting project as a historic furnishings consultant, which is another service I provide in my firm, where I assisted in the recreation of a mid-20th century period interior. In my 2018 appraisal work I had the pleasure of working with a diverse group of clients including private collectors, insurance agencies, and corporations, and I thank them for the opportunity to assist with the protection of their collections.